Download Types of Accounts - Lecture - Accounting - Dr. Kalra and more Lecture notes Accounting in PDF only on Docsity!

FINAL ACCOUNTS

There are three following stages of preparing final

accounts of a trading concern:

1. Trading Account

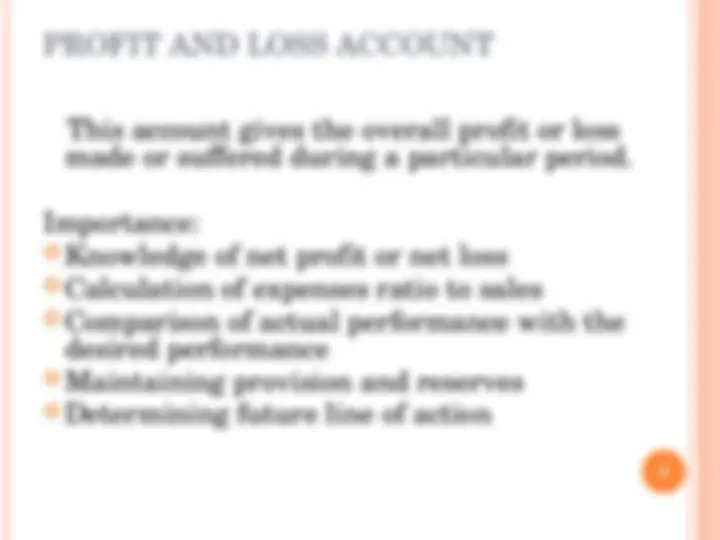

2. Profit and Loss Account

3. Balance Sheet

Manufacturing concerns prepare Manufacturing

Account also before preparing Trading Account

1

TRADING ACCOUNT

Gross profit or Gross loss is ascertained by preparing

Trading A/c.

Cost of goods sold = opening stock+ Net purchases+ Direct

expensesClosing stock

Importance and purpose of preparing Trading A/c:

Ascertaining gross profit or gross loss

Ascertaining ratio of direct expenses to gross profit

Calculation of gross profit ratio

Comparison of stock with the stock of previous year

Comparing the actual performance with the desired

performance

Comparing the actual performance with the previous

performance 2

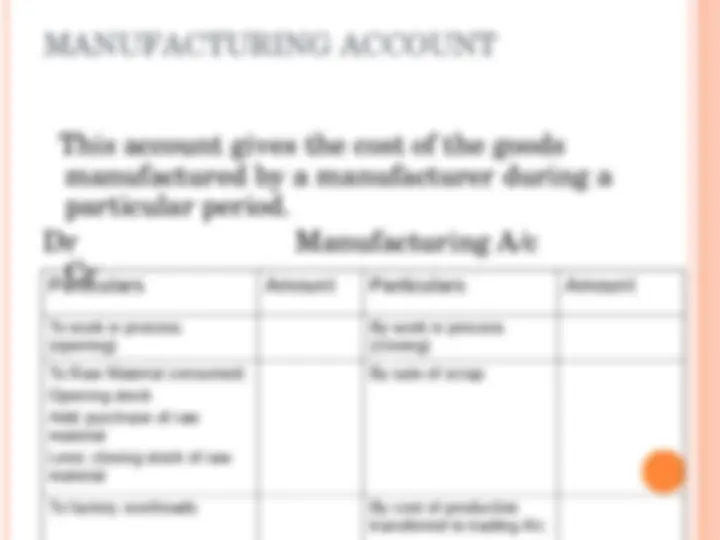

MANUFACTURING ACCOUNT

This account gives the cost of the goods manufactured by a manufacturer during a particular period. Dr Manufacturing A/c Cr

Particulars Amount Particulars Amount

To work in process (opening) By work in process (closing) To Raw Material consumed: Opening stock Add: purchase of raw material Less: closing stock of raw material By sale of scrap To factory overheads By cost of production transferred to trading A/c^4

BALANCE SHEET

‘A balance sheet is a mirror which reflects the

true position of assets and liabilities on a

particular date.’

Assets = Liabilities + Capital

Characteristics:

Balance sheet is a statement

Prepared on a specified date

It is a statement of assets and liabilities

Knowledge about the nature of assets and

liabilities

Knowledge of financial position

Assets and Liabilities tally each other

5

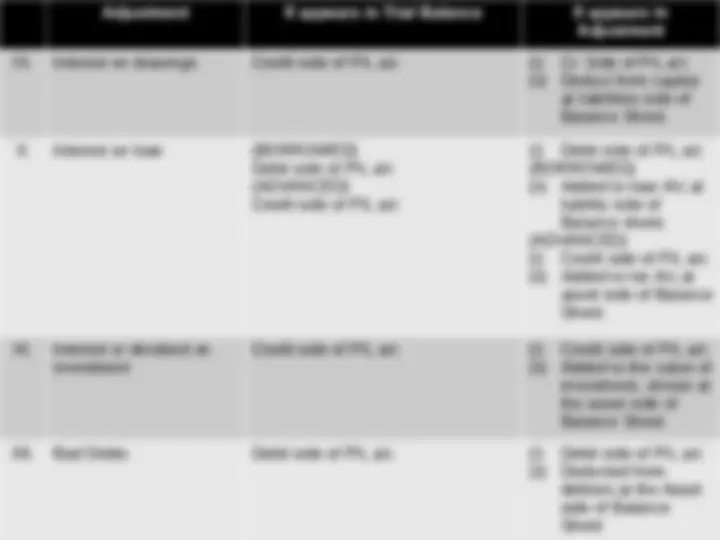

7 While preparing final accounts, at the end of every accounting period, we come across certain problems. The accountant may come to know of certain adjustments to be made in the books of accounts to give a true picture of the state of affairs of the business after closing the books of accounts. These adjustments generally relate to the following: Adjustment If appears in Trial Balance If appears in Adjustment I. Closing stock Cr. Side of trading a/c (i) Cr. Side of trading A/c (ii) Asset side of Balance sheet II. Depreciation Dr. side of P/L a/c (i) Dr. side of P/L a/c (ii) Reduce the value of concerned asset in balance sheet III. Appreciation Cr. Side of P/L a/c (i) Cr. Side of P/L a/c (ii) Increase the value of concerned asset in balance sheet IV. Outstanding Expenses Liability side only in Balance Sheet (i) Added to concerned expense at the debit side of Trading or P/L a/c (ii) Liability side of Balance Sheet

8 Adjustment If appears in Trial Balance If appears in Adjustment V. Prepaid expenses Asset side of Balance Sheet (i) Deduce from concerned expenses at the debit side of Trading or P/L a/c (ii) Asset side of Balance Sheet VI. Outstanding or Accrued income Asset side of Balance sheet (i) Added to the concerned income at the credit side of P/L a/c (ii) Asset side of Balance Sheet VII. Unearned Income Shown at the liabilities side of Balance Sheet (i) Deduct from the concerned income at the credit side of P/L a/c (ii) Shown at liabilities side of Balance Sheet. VIII. Interest on capital Debit side of the P/L a/c (i) Dr. side of P/L a/c (ii) Increase amount of capital at the liabilities side of

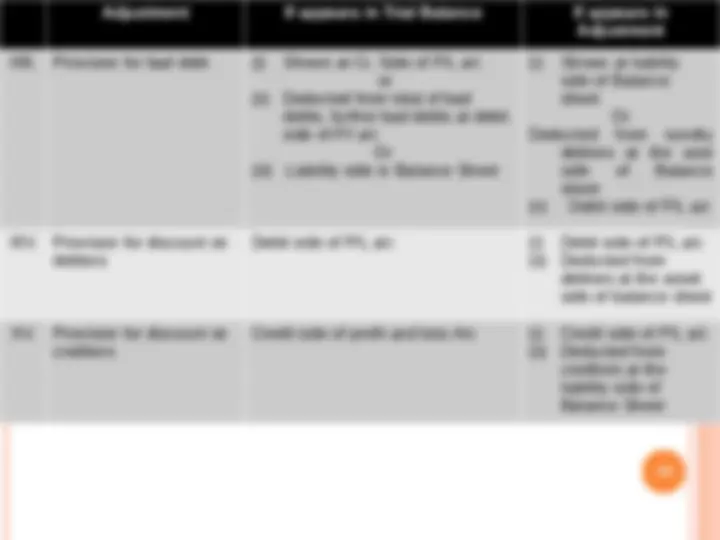

10 Adjustment If appears in Trial Balance If appears in Adjustment XIII. Provision for bad debt (i) Shown at Cr. Side of P/L a/c or (ii) Deducted from total of bad debts, further bad debts at debit side of P/l a/c Or (iii) Liability side in Balance Sheet (i) Shown at liability side of Balance sheet Or Deducted from sundry debtors at the asst side of Balance sheet (ii) Debit side of P/L a/c XIV. Provision for discount on debtors Debit side of P/L a/c (i) Debit side of P/L a/c (ii) Deducted from debtors at the asset side of balance sheet XV. Provision for discount on creditors Credit side of profit and loss A/c (i) Credit side of P/L a/c (ii) Deducted from creditors at the liability side of Balance Sheet

THE FOLLOWING IS THE TRIAL BALANCE OF

ST

MARCH 1993:

____________________________________________________________________________ 353160 353160

- MR. KAPUR ON - Cash in hand Rs. Debit Credit - Cash at bank - Purchases - Sales - Returns - Wages - Fuel and power - Carriage on sales - Carriage on purchases - Stock (1492) - Buildings - Freehold land - Machinery - Salaries - Patents - General expenses

- Insurance - Capital 1,42, - Drawings 10, - Sundry debtors

THE FOLLOWING IS THE TRIAL BALANCE OF SRI OM AS ON 31ST^ MARCH, 1999. YOU ARE REQUESTED TO PREPARE THE TRADING AND PROFIT AND LOSS A/C FOR THE YEAR ENDED 31ST^ MARCH1999 AND BALANCE SHEET AS ON THAT DATE Particulars^ AFTER MAKING THE NECESSARY ADJUSTMENTS Debit ( Rs.) : Credit (Rs.) Sundry debtors Sundry creditors Outstanding expenses Wages Carriage outwards Carriage Inwards General Expenses Cash Discounts Bad debts Motor car Printing and stationery Furniture and fittings Advertisement Insurance Salesmen’s commission Postage and telephone Salaries Rates and taxes Drawings Capital Account Purchases Sales Stock on 1.4. Cash at Bank Cash in hand 500000 55000 100000 110000 50000 70000 20000 10000 240000 15000 110000 85000 45000 87500 57500 160000 25000 20000 1550000 2, 60000 10500 36,30, 200000 14,43, 19,87, 36,30, 13

The following adjustments are to be made:

1. Stock on 31st^ March 1999 was valued at Rs.7,25,

2. A provision for bad and doubtful debts is to be created to the

extent of 5% on sundry debtors

3. Depreciate:

Furniture and fittings by 10%

Motor car by 20%

4. Shri Om had withdrawn goods worth Rs.25000 during the year

5. Sales include goods worth Rs.75000 sent out to Shanti& co. on

approval and remaining unsold. The cost of the goods was

Rs.

6. The salesmen are entitled to a commission of 5% on total sales

7. Debtors include Rs.25000 bad debts

8. Purchases include purchase of furniture worth Rs.

14

CAUSES FOR DEPRECIATION:

By constant use

By expiry of time

By obsolescence

By depletion

Permanent fall in price

By accidents

Importance or need for providing depreciation :

For determination of net profit or loss

For showing assets at fair prices and true value in the

balance sheet

Provision for funds in the replacement of assets

Ascertaining accurate cost of production

Distribution of dividend out of profit only

Avoiding over payment of income tax

16

METHODS OF PROVIDING

DEPRECIATION:

Fixed installment method

Diminishing balance method

Annuity method

Depreciation fund method

Insurance policy method

Revaluation method

Depletion method

Machine hour rate method

Sum of years digit method

Replacement method

17

Machinery A/c Dr. Cr. Date Particulars J.F. Amount Date Particulars J.F. Amount 1 st^ july 1993 To bank A/c 40000 Dec 31 1993 By depreciation (on 40000 for six months) 2000 Dec31 By bal c/d 38000 40000 40000 19

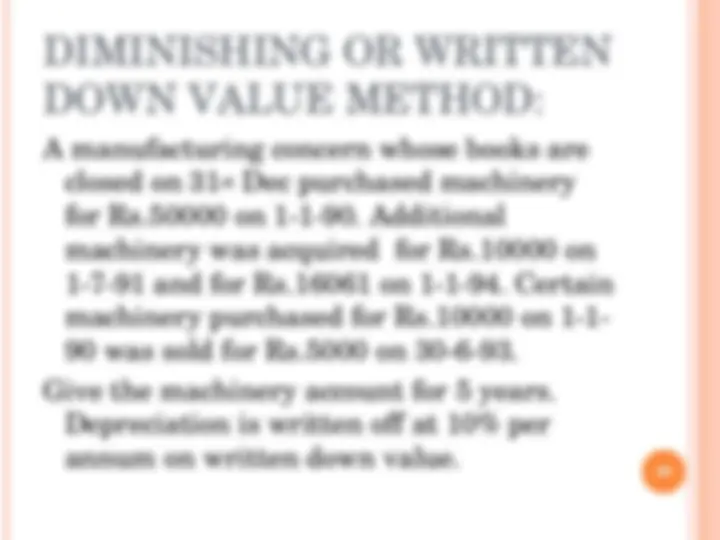

DIMINISHING OR WRITTEN

DOWN VALUE METHOD:

A manufacturing concern whose books are

closed on 31st^ Dec purchased machinery

for Rs.50000 on 1190. Additional

machinery was acquired for Rs.10000 on

1791 and for Rs.16061 on 1194. Certain

machinery purchased for Rs.10000 on 11

90 was sold for Rs.5000 on 30693.

Give the machinery account for 5 years.

Depreciation is written off at 10% per

annum on written down value.

20