Exponential Distribution

• The probability density function of the exponential

distribution is given by

• E[X] = 1/λ

• λ = 1/µ

• Var(X) = 1/λ2

() 0, 0

x

fx e x

λ

λλ

−

=>>

3%

0

() () 1 0, 0

x

x

Fx f xdx e x

λλ

−

==−>>

∫

f(x)%%

x%%

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

The main points i the stochastic hydrology are listed below:Exponential Distribution, Probability Density Function, Exponential Distribution, Expected Time, Gamma Distribution, Scale Parameter, Skewness Coefficient, Shape Parameter, Independent Gamma, Extreme Value Distributions

Typology: Study notes

1 / 27

This page cannot be seen from the preview

Don't miss anything!

x

λ λ λ −

3 0

x x

λ λ −

f(x) x

F(5) = 1 – e -5/ = 0. F(3) = 1 – e -3/ = 0. P[3 < X < 5] = 0.7135 – 0.5276 = 0.

1

x

η η λ λ λ η η − −

7 η η 1 0 t

η ∞ − −

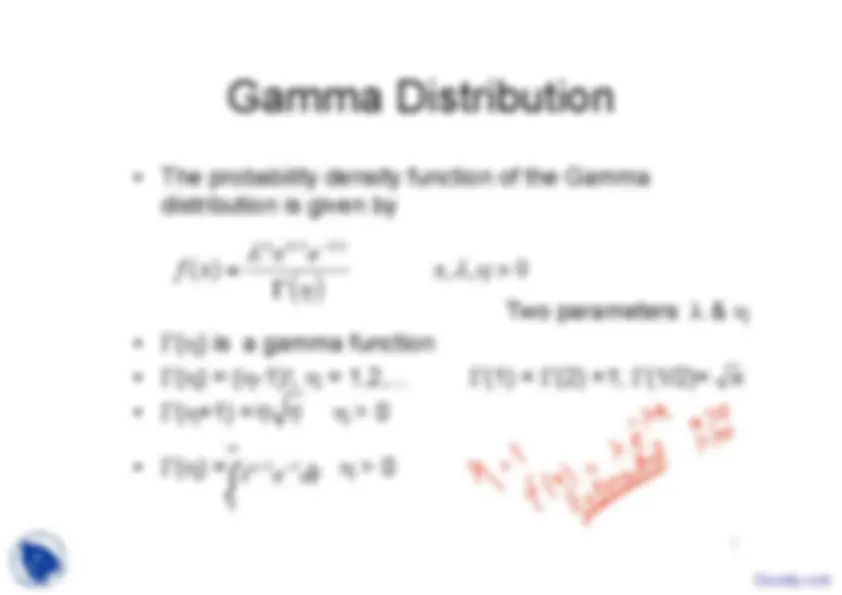

Two parameters λ & η Γ(1) = Γ(2) =1; Γ(1/2)= π

9 η= λ= η= λ=1/ η= λ= η= λ= η=0. λ= x f(x) λ → Scale parameter η → Shape parameter Gamma distribution is in fact a family of distributions

σ 1

η 1

λ 1 = η 1

Example-2 (contd.) 12 1/ 1 η =1. ( ) ( ) 1 1 1 1 1 1 1 1 1 2 2 1 4 4

x X x x

η η λ

− − − − −

1 1

Example-2 (contd.) 13 1 4 0 4

x

−

∫

σ 2

η 2

λ 2 = η 2

Example-2 (contd.) 15 1/ 2

( ) ( ) 2 2 2 2 1 2 2 2 2 4 4 1 4 3 4

x X x x

η η λ

− − − − −

2 2 η λ 2 2 2 2

x

−

∫

1

2

1

2

x

−

∫

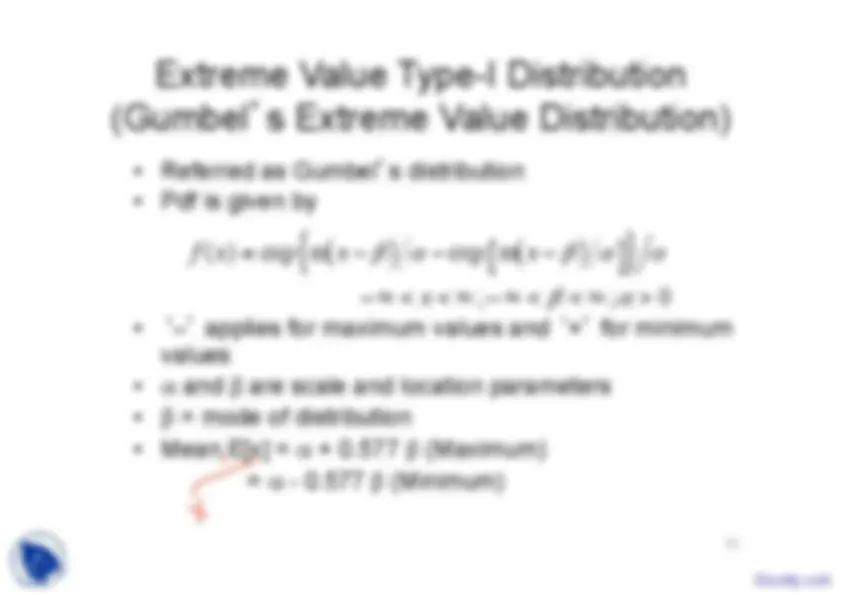

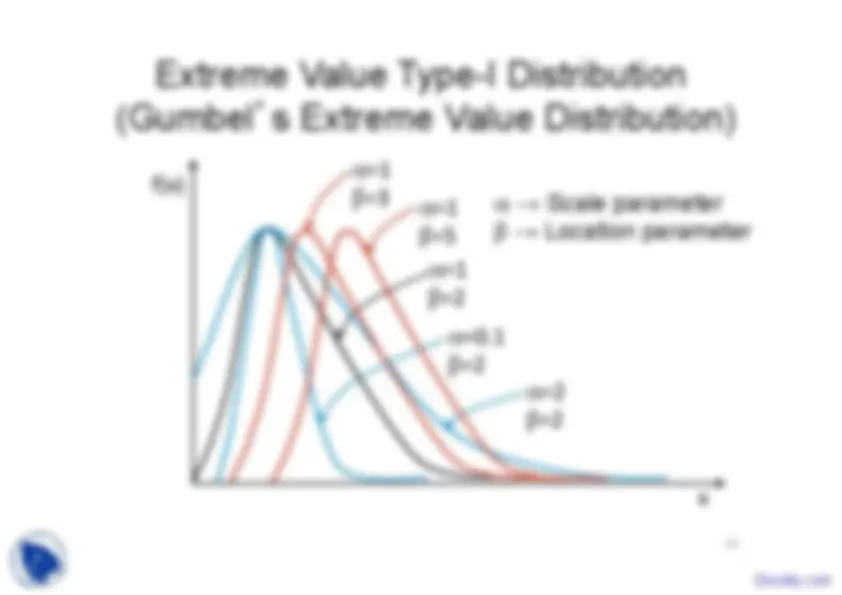

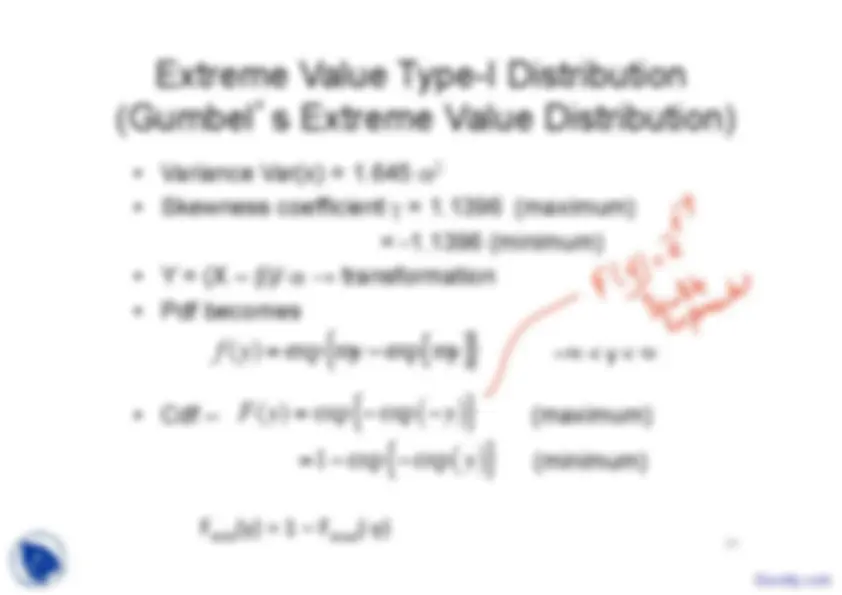

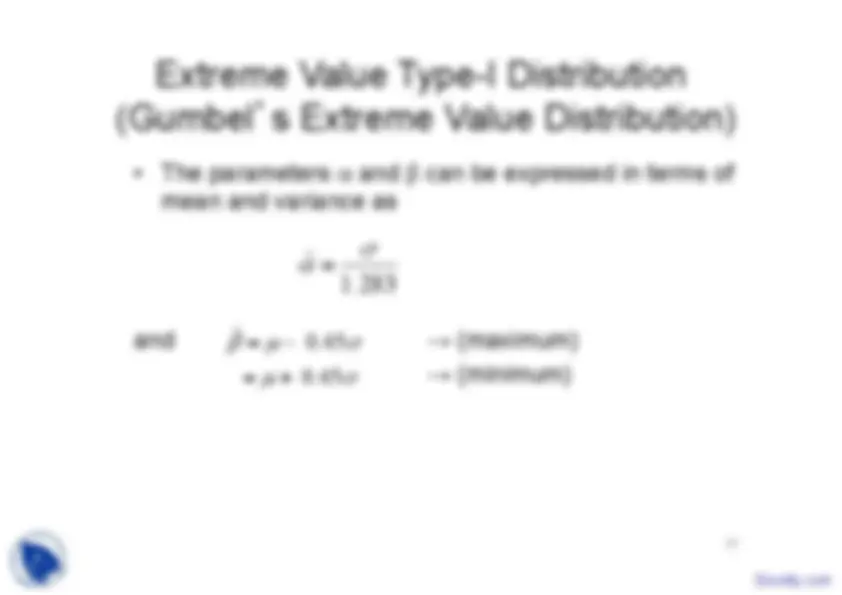

Extreme Value Type-I Distribution (Gumbel s Extreme Value Distribution)