Adjusting Entries

CHAPTER 4

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

The concept of adjusting entries in accounting and their importance in updating accounts to reflect correct balances. It lists the different types of adjustments and their effects if not made. The document also provides examples of adjusting entries for accrued income, accrued expenses, depreciation expenses, and bad debts expenses. It is a useful resource for accounting students to understand the process of adjusting entries and their application in accounting.

Typology: Study notes

1 / 11

This page cannot be seen from the preview

Don't miss anything!

Adjusting Entries Adjusting journal entries are made to update the accounts and bring them their correct balances. The preparation of adjusting entries is an application of the accrual concept of accounting. At the end of the accounting period, some income and expenses may have not been recorded, taken up or updated; hence, there is a need to update the accounts.

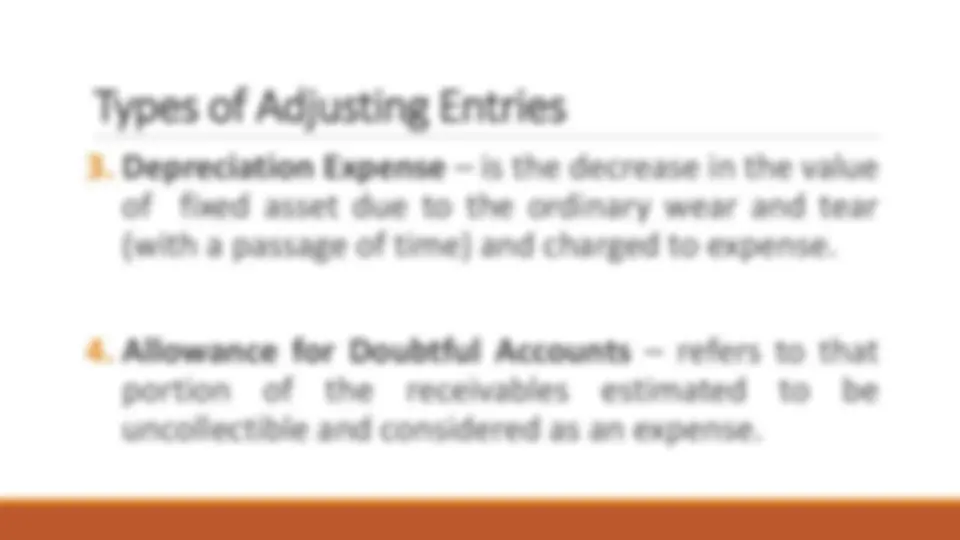

3. Depreciation Expense – is the decrease in the value of fixed asset due to the ordinary wear and tear (with a passage of time) and charged to expense. 4. Allowance for Doubtful Accounts – refers to that portion of the receivables estimated to be uncollectible and considered as an expense. Types of Adjusting Entries

Making the Adjustments Type of Adjustment Adjusting Entry Effects if Adjustment is not made

1. Accrued Revenue Debit Asset Assets under, Owner’s Equity under Credit Revenue Revenue under, Profit under 2. Accrued Expense Debit Expense Expenses under, Profit over Credit Liability Liability under, Owner’s Equity over 3. Unearned Revenue Debit Liability Liability over, Owner’s Equity under Credit Revenue Revenue under, Profit under 4. Prepaid Expense Debit Expense Expenses under, Profit over Credit Asset Asset over, Owner’s Equity over 5. Depreciation Expense Debit Expense Expenses under, Profit over Credit Contra Asset Asset over, Owner’s Equity over 6. Doubtful Accounts Expense Debit Expense Expenses under, Profit over Credit Contra Asset Asset over, Owner’s Equity over

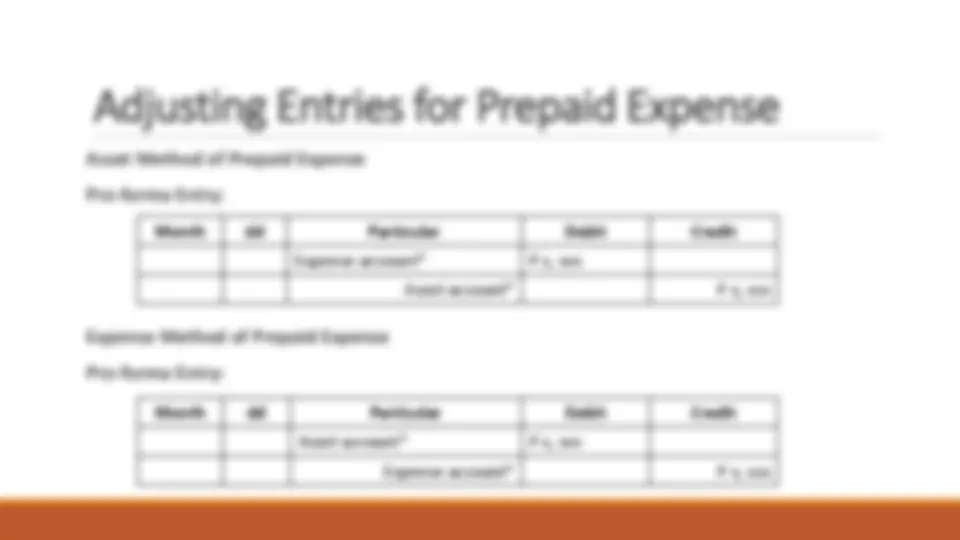

Adjusting Entries for Accrued Expense

Month dd Particular Debit Credit Expense account* P x, xxx Liability account* P x, xxx Month dd Particular Debit Credit Dec. 31 Utilities Expense P1, 800 Utilities Payable P1, 800

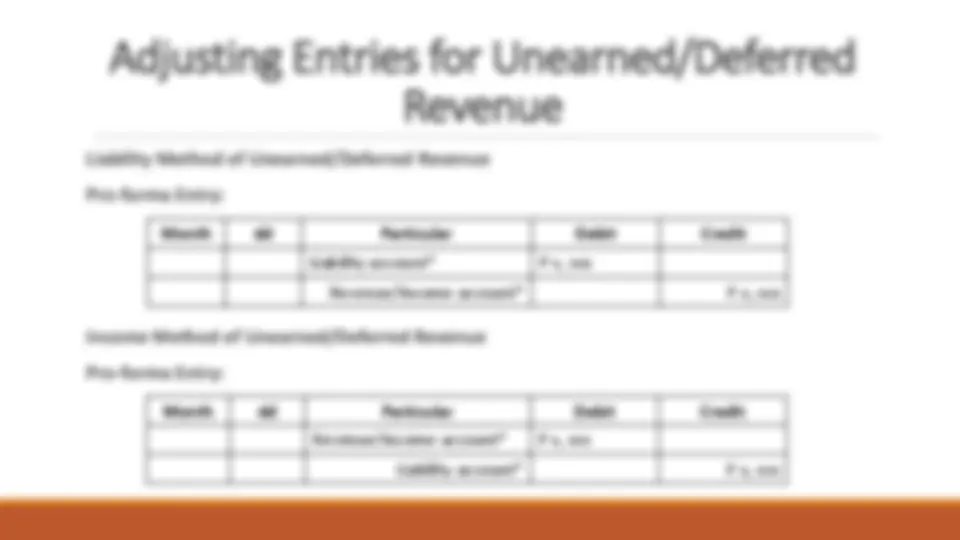

Adjusting Entries for Unearned/Deferred Revenue

Month dd Particular Debit Credit Liability account* P x, xxx Revenue/Income account* P x, xxx Month dd Particular Debit Credit Revenue/Income account* P x, xxx Liability account* P x, xxx

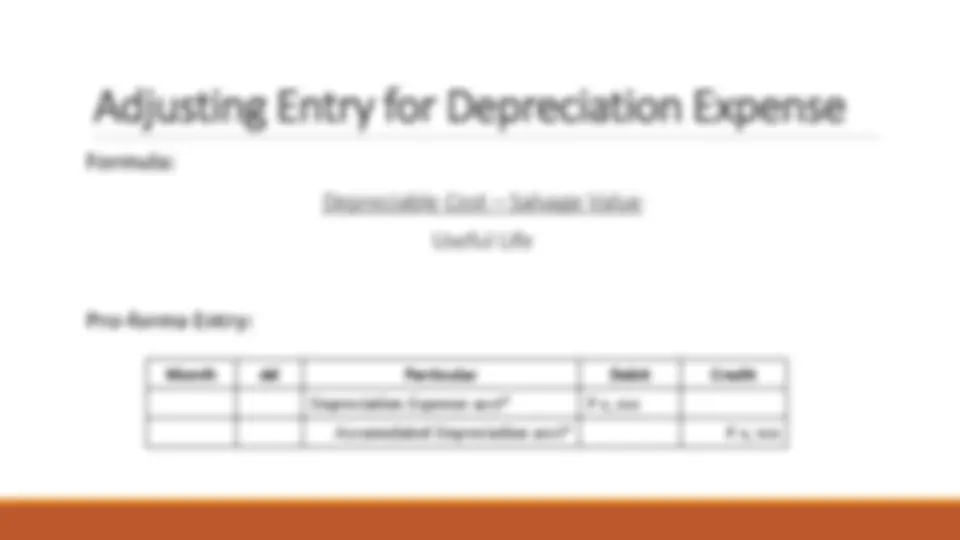

Adjusting Entry for Depreciation Expense

Month dd Particular Debit Credit Depreciation Expense acct* P x, xxx Accumulated Depreciation acct* P x, xxx

Adjusting Entry for Bad Debts Expense

Month dd Particular Debit Credit Doubtful Accounts Expense acct.* P x, xxx Allowance for Doubtful acct.* P x, xxx Month dd Particular Debit Credit Bad Debts Expense* P x, xxx Allowance for Bad Debts* P x, xxx